Ever since the financial crisis of 2007-08, the alternative lending industry has been booming. P2P and fintech lenders and challenger banks have stepped in to provide SMEs with quick access to capital on flexible terms.

Now, post-pandemic, the case for alternative lending is proving even stronger. With high inflation rates and a rising interest rate economy, businesses and consumers are seeking alternative sources of capital to keep up with expenses.

Don’t just take our word for it!

Here are 28 alternative lending statistics and trends, within the US and globally, which show that the industry is thriving, and still has room to grow.

US Alternative Lending Statistics

1. In the US, the total transaction volume of the alternative lending segment is $73.62 billion, up 43% from 2019 ($51.52 billion)

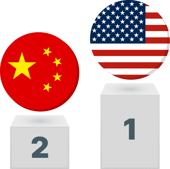

2. The US superseded China as the largest alternative lending market in 2018. As of 2020, the US accounts for 65% of the global alternative finance market value.

3. Within alternative lending, in 2021, the loan origination segment of the industry received the highest revenue share at 21%.

4. As of 2020, the US accounts for over 90% of the alternative lending market share in the Americas.

5. According to a 2022 Business Insider report, the big 5 US banks account for just 21% of mortgage origination, declining from a 50% share in 2011.

6. In 2020, the total volume of alternative loans originated by domestic firms in the US was $72.27 billion—43% higher than in 2019.

7. According to the US Small Business Administration (SBA), Fintechs contributed 3.5% ($28 billion) of the total $799 billion of Paycheck Protection Program (PPP) loans during the Covid-19 crisis between 2020 and 2021.

8. Balance sheet business lending is the largest alternative business lending model in the US. It accounted for a total volume of $22.5 billion, growing 69% Y-o-Y from 2019.

9. The P2P/Marketplace business lending model grew significantly by 455% between 2019 and 2020 and is the second largest business lending model (after balance sheet business lending) with a volume of $8.27 billion..

10. The business alternative lending segment, although smaller than the consumer lending segment, grew by 108% between 2019 and 2020.

11. Between 2019 and 2020, the volume of alternative finance loans for businesses rose by 124% year on year. This counts for over 604,000 transactions and is over 43% of all US alternative finance in the year.

12. In business alternative lending, debt-based alternative lending is the most prevalent segment, representing over 98% of the volume of loans.

13. For a small business, the approval rate for loans from banks is between 14.3% and 20.1%, while the approval rate for loans from alternative lenders is 26.1% (pre-pandemic, this figure was 56.3%!).

14. According to a Federal Reserve Banking report, only 58% of SMB loan requests were approved by banks, while 71% were approved by alternative lenders.

Global Alternative Lending Statistics

1. The global transaction volume of the alternative lending segment reached $113.67 billion in 2020.

2. According to a report by Grandview Research, the compound annual growth rate (CAGR) of the global alternative lending market is projected to be 23.6% from 2022 to 2030.

3. China was the largest alternative lending market holding 71% of the market share, but by 2020 their market share fell to just 1%. This drastic decline is attributed to the Covid-19 pandemic as well as the Chinese government tightening regulatory restrictions on alternative lending after high levels of fraud and default.

4. The SME Finance Forum reported that in 2018, there was a $5 trillion gap between the financing needs of SMEs and the capital allocated for lending by traditional institutions.

This was cited as one of the primary reasons for SMEs to seek alternative sources of finance.

5. A 2019 Business Insider study found that SMEs make up over 99.9% of businesses in the private sector in both the UK and the US.

6. SMEs employ 60% of all workers in the US and 48% of all workers in the UK. SMEs also constitute a significant portion of employment in Organization for Economic Co-operation and Development (OECD) countries, with a recent study claiming that between 50% and 60% of employment is in SMEs.

7. In Europe, in 2021, there were 443 alternative lending deals, a Y-on-Y increase of 79%.

8. Alternative lenders contributed 9.1% (£59.8 billion) of the UK SMB lending market in 2021, up 7.1% from 2018.

9. The SME lending market capitalization in Germany, the 2nd largest alternative lending market in Europe, is set to jump from $303.5m in 2022, to $325m in 2026.

10. Embedded banking (incorporating traditional banking features into non-financial platforms) for SMEs could constitute up to 26% of SME banking revenue by 2025, generating nearly $124 billion.

11. In the UK, fintechs, including P2P or marketplace platforms constituted more than 20% of the Coronavirus Business Interruption Loan Scheme (CBILS) loans issued.

12. The UK ranked as the third-largest alternative lending market in 2020, and is expected to reach £3.5 billion by 2022. The UK also accounts for 56% of the European market in terms of value.

13. Globally, balance sheet business lending was reported to have the second-highest transaction value of $28 billion in 2020 (doubling from the previous year)

14. In 2019, the volume of global online alternative finance (excluding China) that went toward SMEs was $35 billion, up 13% Y-o-Y. In 2020, this increased by 51% Y-o-Y to $53 billion.

The rise in popularity of loan origination software can be attributed to more businesses applying for loans from alternative lenders, especially students and younger professionals applying for personal and education loans.

Alternative lenders are riding the wave of automation and scaling their operations with powerful software. In 2022, the leading alternative lenders are automating not only loan origination but also other stages of the lending lifecycle, including credit decisioning, underwriting and loan fulfillment.

Leverage Technology To Expand Your Lending Operations

Alternative lending is becoming a mainstream source of capital for SMEs, both globally and within the US.

An objective analysis of the numbers leads to the conclusion that demand is only likely to increase–expect more business to come your way. If your lending operation is not capable of handling the additional volume with the same efficiency, you could lose out on this massive opportunity. The key? Doubling down on the digital transformation of your lending business.

Visit Onyx IQ to learn more about the future of lending technology and the state of the SME alternative lending market.